How much should you have saved for retirement?

Katherine Tierney, CFA®, CFP®, Senior Retirement Strategist

October is National Retirement Security Month, and with year-end rapidly approaching, it serves as a good reminder to review your progress toward what is likely one of your most important financial goals — your retirement.

The amount you should have for retirement depends on several factors: how much income you earn and save today, how your investments perform, and how much you plan to spend in retirement and for how long. To give you a sense of where your retirement savings should be at your current age and salary, we've developed general ranges using broad assumptions.

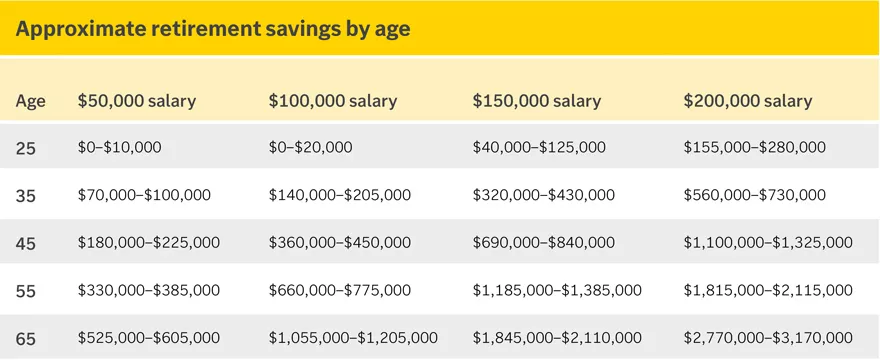

Approximate retirement savings by age

This chart shows the approximate amount an investor should have in their retirement savings based on their approximate age and income. For example, the higher your income and the older you are, the more you should have saved.

This chart shows the approximate amount an investor should have in their retirement savings based on their approximate age and income. For example, the higher your income and the older you are, the more you should have saved.

If you’re not on track for retirement

If your retirement savings aren’t within range, there may be a good reason for that — your specific goal and strategy may differ from our assumptions. For example, you may be planning to retire later or expect your spending to decrease in retirement. A financial advisor can help you review your progress and, if needed, help you explore ways to ramp up your retirement savings, like:

- Maximizing employer matches if offered by your plan. Employer matches are effectively free money.

- Increasing your contributions by 1% each year, which can be done automatically if your employer plan offers an auto-escalation option.

- Contributing to multiple accounts. If you meet the eligibility requirements for each account type, you can contribute up to the annual limit for your employer plan, an IRA and a health savings account (HSA).

- Considering the backdoor Roth strategy if your income exceeds the limits for a Roth IRA.

- Taking advantage of catch-up contributions if you’re age 50 or older.

- Using the mega backdoor Roth strategy if you’re already maxing out retirement contributions and your employer plan allows for it.

If you’re already retired

If already retired, be sure to review your strategy with your financial advisor at least annually (or sooner if you experience a life event). Even if your goal and situation haven’t changed much year over year, ever-changing economic conditions mean your portfolio and withdrawal strategy need to be checked regularly.

To help increase the likelihood your money lasts through retirement:

- Be flexible with your spending. Like the retirement savings ranges, your strategy likely assumes your spending will increase annually in retirement. If your current spending meets your needs, though, don’t automatically increase your portfolio withdrawals each year. Forgoing an annual increase, especially following a down market, can meaningfully improve the longevity of your investment portfolio.

- Maintain an appropriate cash balance for planned and unplanned expenses. We recommend holding 12 months of portfolio withdrawals in cash and three to five years of withdrawals in CDs and other short-term fixed income to meet your spending needs. That’s in addition to emergency savings equal to three to six months of spending. Maintaining appropriate cash reserves can help you avoid selling stocks in down markets to meet your spending needs.

- Rebalance your portfolio. Your portfolio allocation may need to shift significantly over the course of retirement. Ensure your portfolio remains aligned to your goal, risk tolerance and time horizon.

Feel more secure in your retirement

Take time this October to check in on your retirement security and revisit your progress. Whether working toward retirement or already retired, your financial advisor can help you tailor a strategy for your unique situation.

Katherine Tierney

Katherine Tierney is a Senior Retirement Strategist on the Client Needs Research team at Edward Jones. The Client Needs Research team develops and communicates advice and guidance for client needs, including retirement, education, preparing for the unexpected and leaving a legacy. Katherine has more than 15 years of financial services and retirement experience. She is a contributor to the Edward Jones Perspectives newsletter and has been quoted in various publications.