Monthly portfolio brief

Approaching year-end on a high note

What you need to know

- After the U.S. elections, markets focused on potential policy shifts and their implications on global growth, inflation and interest rates.

- U.S. equities performed exceptionally well post-election, hitting new all-time highs and generally helping well-diversified portfolios approach year-end on a high note.

- Cyclical investments led the post-election rally, demonstrating broader market leadership amid brighter near-term economic growth prospects and a central bank easing cycle.

- We recommend overweighting equity investments with an eye toward U.S. equities, given our expectation for their outperformance to continue into 2025.

- Know the purpose for the cash you hold. Reducing overweight positions can help you manage reinvestment risk as central banks cut interest rates in the months ahead.

Portfolio tip

Cash allocations can provide stability, but they aren’t risk-free. Put extra cash to work by using your portfolio’s strategic allocations as a guide — they can help you stay focused on your goals.

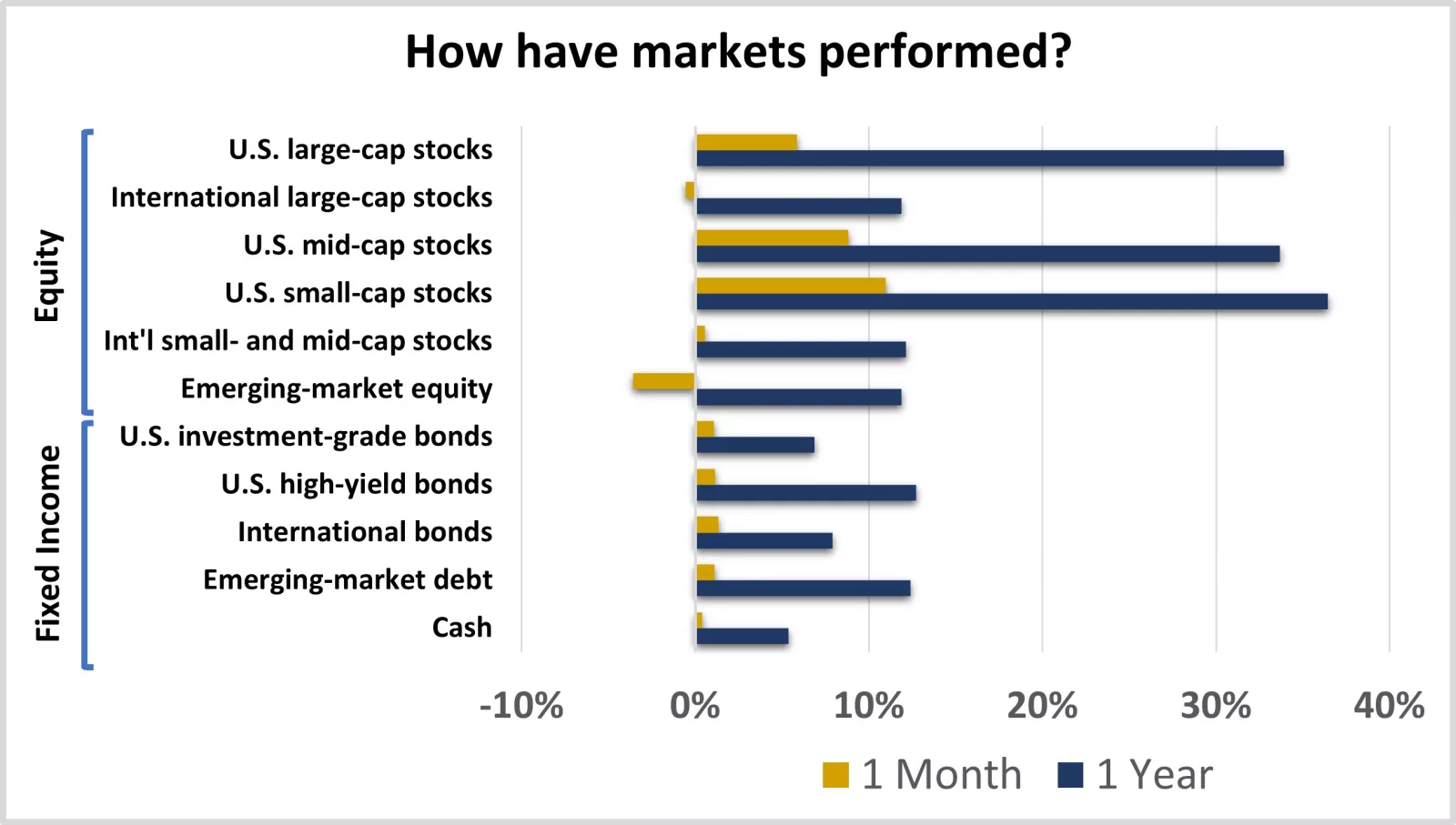

This chart shows the performance of equity and fixed-income markets over the previous month and year.

This chart shows the performance of equity and fixed-income markets over the previous month and year.

Where have we been?

Markets focused on potential policy shifts following the U.S. elections. There’s little debate the U.S. elections and their potential policy implications were among the most attention-grabbing headlines last month, and they captured the market’s focus as well. As the results became clear — a Republican sweep in the White House, Senate and House of Representatives — markets began adjusting to likely policy shifts.

Among them, the higher likelihood for extended tax relief and deregulation has helped brighten the near-term outlook for the U.S. economy. On the flip side, the potential impact on inflation, global growth and interest rates from increasingly restrictive trade and immigration policies and larger deficits drove some concern. These considerations will affect asset classes and sectors differently, but on balance, they helped provide an immediate boost to the ongoing momentum and outperformance of U.S. equities.

U.S. equities performed exceptionally well, led by cyclical investments amid stronger growth prospects. Perhaps it isn’t surprising that, once again, U.S. equities captured the lead in November. They’ve stood out in recent periods, supported by relative economic resilience, rising corporate profits and exciting tech innovations. But under the surface have been signs of broadening and rotation, benefiting well-diversified portfolios.

Cyclical sectors such as financials, industrials and consumer discretionary led the recent rally, with more economically sensitive equity asset classes leading more broadly. Within U.S. large-cap stocks, the financials sector has now outperformed all others over the past 12 months, up nearly 50% during the period.

U.S. small- and mid-cap stocks had the strongest post-election rally among U.S. equities, given their greater sensitivity to economic growth. Both asset classes hit all-time highs in November, helping well-diversified portfolios head toward year-end on a high note.

U.S. small-cap stocks have now been the best-performing asset class on a 12-month basis, a title that had been held by U.S. large-cap stocks for much of the year. But all three U.S. equity asset classes have performed exceptionally well, demonstrating broader leadership and benefiting portfolios holding overweight U.S. equity positions.

International equity weighed on portfolios amid trade and geopolitical uncertainties. International equities were flat to lower in November as markets considered likely shifts in global policies. Emerging-market equity dropped the most, pulled lower by underperformance within Chinese stocks due partially to the greater expectation for higher tariffs.

More broadly, the dollar strengthened on U.S. growth prospects and higher interest rates. A stronger dollar weighs on returns from international equities. But even with November’s weakness, international equities have enjoyed solid double-digit returns over the past 12 months.

Bonds provided a slight boost as yields trended lower toward month-end. Interest rates had ticked higher in recent months on expectations some central banks, such as the Federal Reserve, may take a more cautious approach to rate cuts, given still-solid economic growth and still-elevated inflation. But the late-month interest rate descent, recurring interest income and contained credit spreads helped bonds eek out gains in November. Zooming out, one-year gains across all fixed-income asset classes are impressive, as they are across equities.

What do we recommend going forward?

Know the purpose for the cash you hold and reduce overweight positions. Cash, money market funds and short-term bond investments can play an important role in your financial strategy, such as serving as your emergency funds or helping you manage short-term spending needs. It’s important to align your cash needs with your cash allocations to ensure you have enough but not too much. When reviewing an investment portfolio designed for longer-term goals such as retirement, we recommend limiting cash and cash equivalents to no more than 5%, and we place our target at 1% specifically.

With inflation likely contained and economic momentum moderating, we expect central banks to continue normalizing monetary policies. Yields on short-term bond and cash-like investments are likely to follow closely central bank rate cuts, highlighting the reinvestment risk of these investments. And over the long term, we expect cash returns to lag all other recommended asset classes.

While cash can provide stability for a portfolio and serve as a source of investment, we recommend reducing overweight positions in this environment. Use your portfolio’s strategic allocations as a guide when putting extra cash to work — they can help you stay focused on your goals.

Slightly underweight fixed-income investments, but increase the interest rate sensitivity of bond allocations. Higher interest rates have increased the attractiveness of bonds, given the greater interest income and diversification benefits they provide a portfolio. Although likely not as fast nor as far as previously expected for some, multiple major central banks are likely to cut rates further, which could benefit bond returns.

However, the potential for bond price appreciation may be limited if economic growth remains sound and the disinflation trend slows, as we expect. Therefore, we believe the backdrop is more favorable for stocks, and we recommend slightly higher equity allocations, relative to your long-term targets.

We believe investment opportunities exist within fixed-income markets, despite our recommendation to underweight. Given the ongoing central bank rate-cutting cycle, we continue to believe it’s beneficial to increase the interest rate sensitivity of a bond portfolio, particularly when allocating toward bond markets with relatively attractive valuations. Consider slightly reallocating from U.S. high-yield bonds toward emerging-market debt. Credit spreads within emerging-market debt are more appealing, and the asset class is generally higher in quality.

Beyond limiting overweight allocations to cash-like investments, you can further reduce reinvestment risk within your portfolio by slightly lowering short-term U.S. investment-grade bond allocations, reallocating toward intermediate- or longer-term maturities. This could help increase the interest rate sensitivity of your portfolio and help you lock in higher interest rates for a longer period.

Overweight U.S. equities; they should benefit from U.S. economic and market momentum. Within our recommendation to overweight equity investments, we favor U.S. large- and mid-cap stocks. We expect U.S. stocks to be supported by the demonstrated and ongoing strength of the domestic economy and corporate profits, particularly when compared to other developed economies.

Policy shifts such as higher tariffs and immigration restrictions may weigh on growth over time, but their timing and size remain uncertain. Once they’re implemented, it is likely to take time for their full impact to filter through the economy. With solid fundamentals in place, we believe it’s likely we’ll see additional new high notes within U.S. equities in 2025, even if gains slow from an exceptional pace.

Broadening market leadership amid a central bank rate-cutting cycle could also help U.S. stocks continue to outperform. Slightly reallocating from U.S. investment-grade bonds and international developed-market stocks toward U.S. large- and mid-cap stocks can help you maintain a level of quality within your portfolio, while benefiting from more cyclical investments amid supportive U.S. growth.

We’re here for you

If you’re looking for ways to end your year positively, consider a portfolio review with your financial advisor, basing the conversation on your personal circumstances and tax considerations. Our strategic asset allocation guidance is designed to help you create a solid foundation for a well-diversified, goal-focused investment strategy, and our opportunistic portfolio guidance is designed to help smoothly transition your investment portfolio into 2025.

If you don’t have a financial advisor and would like to build an investment strategy aligned with your financial goals, we invite you to meet with an Edward Jones financial advisor.

Strategic portfolio guidance

Defining your strategic investment allocations helps to keep your portfolio aligned with your risk and return objectives, and we recommend taking a diversified approach. Our long-term strategic asset allocation guidance represents our view of balanced diversification for the fixed-income and equity portions of a well-diversified portfolio, based on our outlook for the economy and markets over the next 30 years. The exact weightings (neutral weights) to each asset class will depend on the broad allocation to equity and fixed-income investments that most closely aligns with your comfort with risk and financial goals.

Diversification does not ensure a profit or protect against loss in a declining market.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: U.S. large-cap stocks, international large-cap stocks, U.S. mid-cap stocks, U.S. small-cap stocks, international small- and mid-cap stocks, emerging-market equity.

Fixed-income diversification: U.S. investment-grade bonds, U.S. high-yield bonds, international bonds, emerging-market debt, cash.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: U.S. large-cap stocks, international large-cap stocks, U.S. mid-cap stocks, U.S. small-cap stocks, international small- and mid-cap stocks, emerging-market equity.

Fixed-income diversification: U.S. investment-grade bonds, U.S. high-yield bonds, international bonds, emerging-market debt, cash.

Opportunistic portfolio guidance

Our opportunistic portfolio guidance represents our timely investment advice based on current market conditions and a shorter-term outlook. We believe incorporating this guidance into a well-diversified portfolio may enhance your potential for greater returns without taking on unintentional risks, helping keep your portfolio aligned with your risk and return objectives. We recommend first considering our opportunistic asset allocation guidance to capture opportunities across asset classes. We then recommend considering opportunistic equity style, U.S. equity sector and U.S. investment-grade bond guidance for more supplemental portfolio positioning, if appropriate.

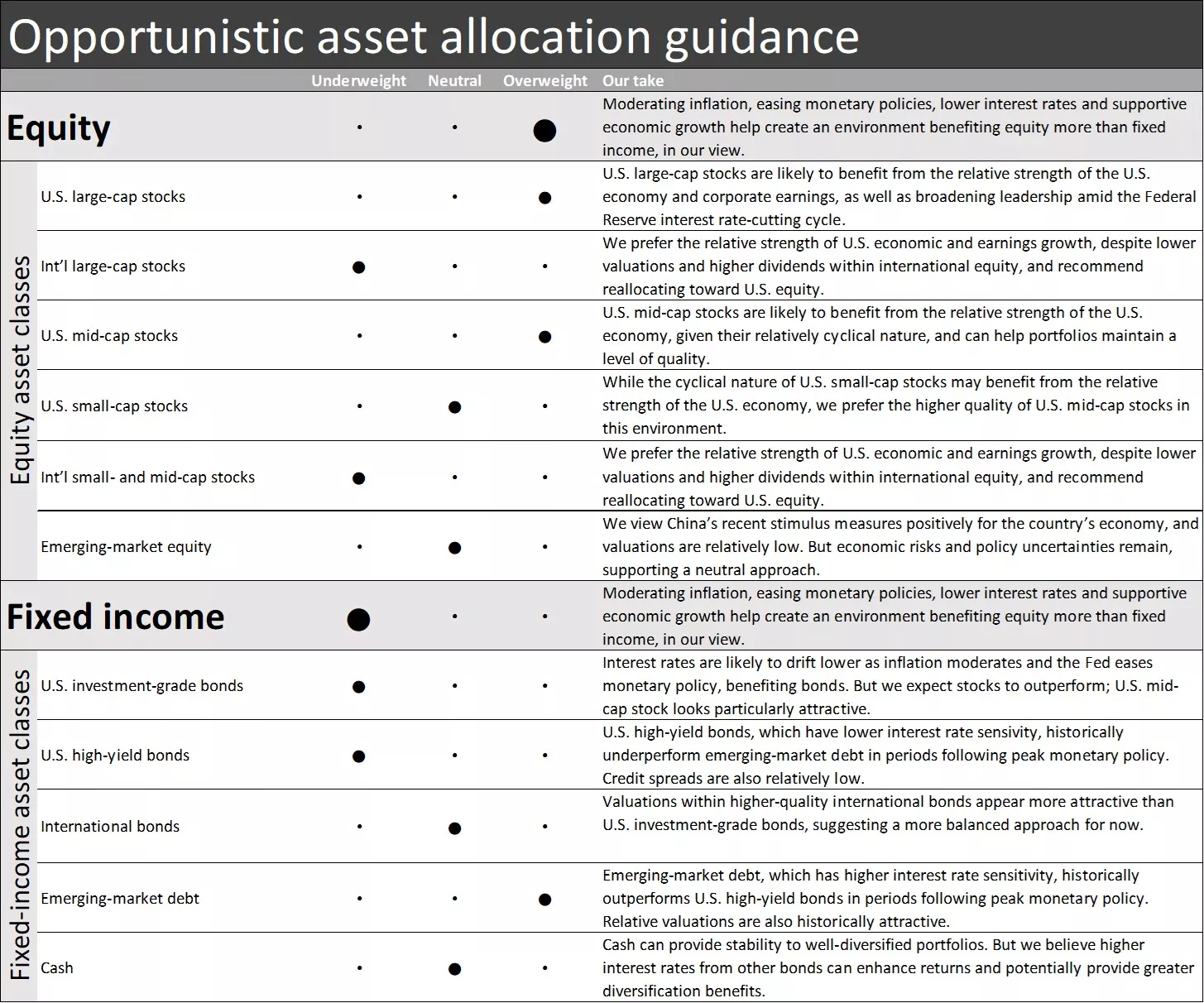

Our opportunistic asset allocation guidance follows:

Equity — overweight overall; overweight for U.S. large-cap stocks and U.S. mid-cap stocks; neutral for U.S. small-cap stocks and emerging-market equity; underweight for international large-cap stocks and international small- and mid-cap stocks.

Fixed income — underweight overall; overweight for emerging-market debt; neutral for international bonds and cash; underweight for U.S. investment-grade bonds and U.S. high-yield bonds.

Our opportunistic asset allocation guidance follows:

Equity — overweight overall; overweight for U.S. large-cap stocks and U.S. mid-cap stocks; neutral for U.S. small-cap stocks and emerging-market equity; underweight for international large-cap stocks and international small- and mid-cap stocks.

Fixed income — underweight overall; overweight for emerging-market debt; neutral for international bonds and cash; underweight for U.S. investment-grade bonds and U.S. high-yield bonds.

Our opportunistic equity style guidance is neutral for value-style equity and growth-style equity.

Our opportunistic equity style guidance is neutral for value-style equity and growth-style equity.

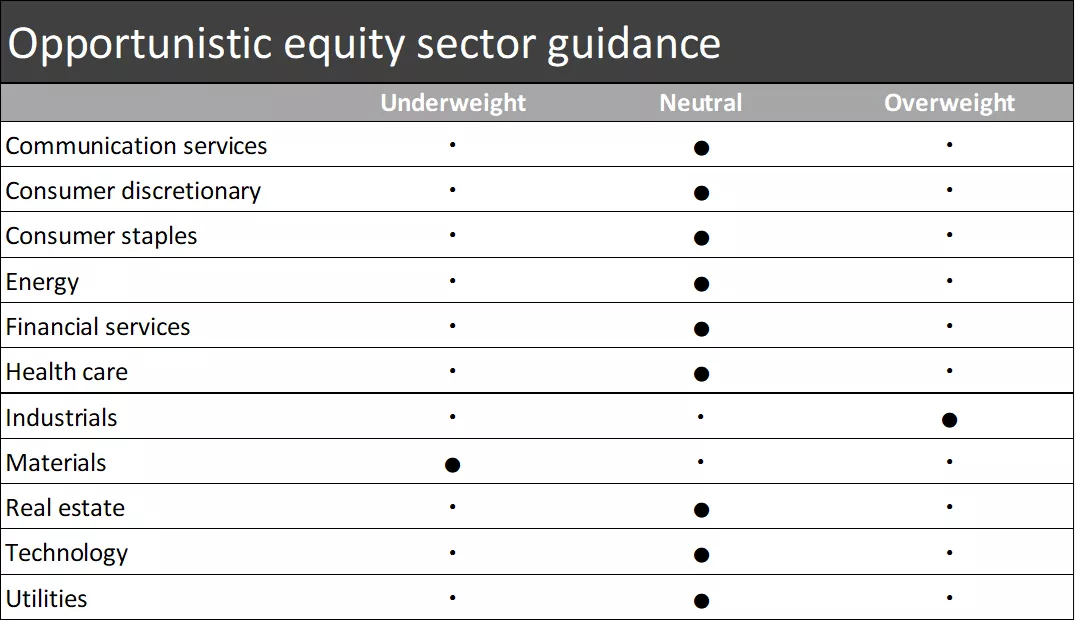

Our opportunistic equity sector guidance follows:

• Overweight for industrials

• Neutral for communications services, consumer discretionary, consumer staples, energy, financial services, health care, real estate, technology and utilities

• Underweight for materials

Our opportunistic equity sector guidance follows:

• Overweight for industrials

• Neutral for communications services, consumer discretionary, consumer staples, energy, financial services, health care, real estate, technology and utilities

• Underweight for materials

Our opportunistic U.S. investment-grade bond guidance is overweight in interest rate risk (duration) and neutral in credit risk.

Our opportunistic U.S. investment-grade bond guidance is overweight in interest rate risk (duration) and neutral in credit risk.

Tom Larm, CFA®, CFP®

Tom Larm is a Portfolio Strategist on the Investment Strategy team. He is responsible for developing advice and guidance related to portfolio construction, asset allocation and investment performance to help clients achieve their long-term financial goals.

Tom graduated magna cum laude from Missouri State University with a bachelor’s degree in finance. He earned his MBA from St. Louis University, is a CFA charterholder and holds the CFP professional designation. He is a member of the CFA Society of St. Louis.

Important information

Past performance of the markets is not a guarantee of future results.

Investing in equities involves risk. The value of your shares will fluctuate, and you may lose principal. Mid- and small-cap stocks tend to be more volatile than large-company stocks. Special risks are involved in international and emerging-market investing, including those related to currency fluctuations and foreign political and economic events.

Diversification does not ensure a profit or protect against loss in a declining market.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity. High-yield bonds carry a high risk of principal loss and may experience more price volatility than investment-grade bonds. Emerging-market bonds are riskier than bonds from more developed countries.

The opinions stated are for general information purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.