Positioning portfolios amid the market rally

What you need to know

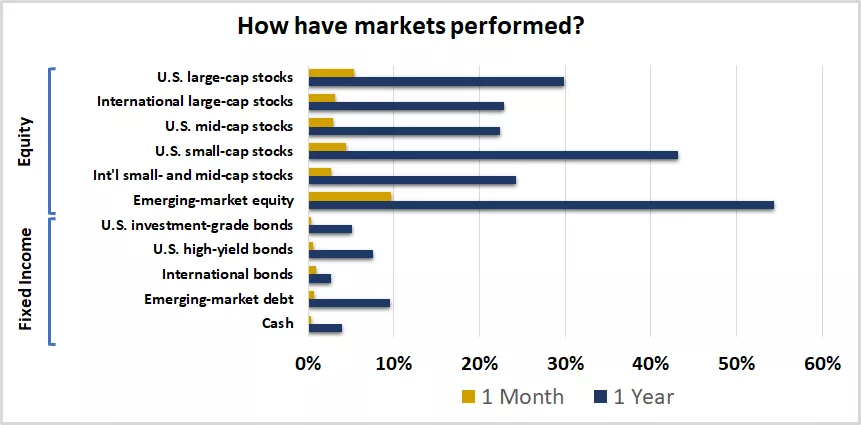

- Equity markets extended their rally in May, driven by strong corporate earnings—particularly in the technology sector—and improving sentiment tied to expectations of a diplomatic resolution to the Iran conflict, which also sent oil prices lower.

- Fixed income also delivered positive returns, led by international bonds as overseas government bond yields declined, amid the fall in oil prices.

- We believe the outlook for global equity markets may remain constructive, supported by resilient economic activity and solid earnings growth.

Portfolio tip

Equities have rallied sharply over the past two months, raising the question of whether markets have gone too far, too fast. Rather than attempting to time market peaks, we recommend investors focus on diversification and maintain a disciplined, goal-oriented investment strategy.

This chart shows the performance of equity and fixed-income markets over the previous month and year.

This chart shows the performance of equity and fixed-income markets over the previous month and year.

Where have we been?

The equity market rally continued in May, supported by strong earnings growth and rising expectations for a diplomatic resolution to the conflict in Iran. Global equities extended April’s momentum, building on a sharp rebound from the March lows. Easing geopolitical tensions supported investor sentiment and pushed WTI crude oil prices down from over $100 per barrel early in the month to below $90 by month-end.

Investors also welcomed solid first-quarter corporate earnings, particularly in the U.S. technology sector. Equity market gains weren't limited to U.S. borders, with international equities also posting solid returns, led by emerging markets. Fixed-income markets delivered positive returns as well, with international bonds outperforming as overseas government bond yields declined alongside falling oil prices.

Strong momentum within the technology sector continued. Within U.S. equities, the technology sector remained the leader in May, rising 16% and more than 40% since the March 30 low. Strong profit growth has been a key driver of the rally, with the S&P 500 technology sector delivering over 50% year-over-year earnings growth in the first quarter, while full-year growth is expected to reach 47%. Outside of technology, performance was more muted, with health care and consumer discretionary the only other sectors to finish higher in May.

Alongside strength in U.S. large-cap tech, economically sensitive segments also performed well. U.S. small- and mid-cap stocks delivered solid returns, supported by resilient economic data. International equities were also firmly higher, led by emerging markets, which rose more than 9% in May and over 50% over the past year. Gains in emerging-markets were led by technology-heavy regions such as Korea and Taiwan, which continue to benefit from strong AI-related spending.

Fixed income held steady with international bonds and credit-sensitive asset classes the top performers. U.S. investment-grade bonds posted a modest gain, despite a rise in Treasury yields following elevated April inflation data, which showed headline CPI rising 3.8% year over year—the highest since 2023. While markets had expected the Fed to lower interest rates entering 2026, expectations have shifted, with traders now anticipating the Fed to remain on hold in 2026 and deliver one interest-rate hike by the end of next year, putting upward pressure on U.S. yields.

International bonds led fixed-income performance, supported by declining government bond yields overseas amid lower oil prices. Credit-sensitive asset classes, including high-yield and emerging-market debt, also delivered positive returns, supported by resilient economic activity and de-escalating geopolitical tensions.

What do we recommend going forward?

Anchor your portfolio to your goals. Over the past year and a half, markets have navigated a steady stream of headlines—from the 2025 trade policy overhaul to the war in Iran and rising oil prices in 2026. Despite this, markets have remained resilient, underscoring the importance of maintaining a disciplined investment approach through periods of uncertainty.

Looking ahead, we believe investors are best served by staying diversified, maintaining discipline, and anchoring portfolios to their long-term goals.

Discuss your risk tolerance, time horizon, and financial goals with your financial advisor as a starting point. These factors should guide your strategic asset allocation—the mix of stocks and bonds aligned with your objectives—which forms the foundation of your portfolio.

- Use opportunistic tilts to position for a healthy fundamental backdrop. Once you've determined the appropriate mix of stocks and bonds for your financial situation, consider the following opportunistic tilts to position portfolios for a healthy fundamental backdrop:

- Overweight stocks. Consider tilting portfolios toward equities by underweighting bonds. In our view, a combination of solid economic growth, a resilient labor market, and strong corporate earnings can create a favorable backdrop for stocks. At the same time, with inflation above the Fed’s 2% target and central banks in Europe and Japan expected to raise interest rates in 2026, we see limited scope for a meaningful decline in bond yields—supporting a relative preference for equities.

Within this equity overweight, we recommend a globally diversified approach, with exposure to both U.S. and international markets:

- Overweight U.S. large- and mid-cap stocks. U.S. economic data has remained resilient despite higher oil prices and geopolitical uncertainty. Job growth has stabilized, with layoffs still limited—evidenced by low initial jobless claims and a contained unemployment rate. Manufacturing activity has also improved, with the ISM manufacturing PMI expanding for five consecutive months. Combined with strong profit growth, this backdrop underpins our constructive view on U.S. large- and mid-cap equities.

- Position for continued international equity momentum. We see attractive opportunities in emerging markets and international small- and mid-cap stocks, which could benefit from easing geopolitical tensions and normalization in global oil supply over time. Emerging-market equities, in particular, are supported by robust AI-driven demand for semiconductors, a meaningful component of the MSCI Emerging Markets Index. In addition, a potential decline in the U.S. dollar amid easing geopolitical pressures could provide further support for international equities.

- Overweight stocks. Consider tilting portfolios toward equities by underweighting bonds. In our view, a combination of solid economic growth, a resilient labor market, and strong corporate earnings can create a favorable backdrop for stocks. At the same time, with inflation above the Fed’s 2% target and central banks in Europe and Japan expected to raise interest rates in 2026, we see limited scope for a meaningful decline in bond yields—supporting a relative preference for equities.

- Stay balanced across the yield curve. U.S. bond yields have risen this year, driven by higher oil prices and persistent inflation, leading to muted returns for U.S. investment-grade bonds. With U.S. economic growth steady, inflation elevated, and the Fed expected to remain on hold in 2026, we view the risk-reward tradeoff between short- and long-term bonds as broadly balanced. In this environment, we recommend maintaining diversified exposure across short-, intermediate-, and long-term U.S. investment-grade bonds.

We’re here for you

Equity markets have rallied in recent months, pushing the March pullback firmly into the rearview mirror. While the remainder of 2026 will likely bring additional uncertainty, we believe investors are best served by maintaining a disciplined approach anchored to their financial goals. Talk with your financial advisor about structuring your portfolio according to your risk and return objectives to help ensure your financial journey can remain consistently pointed toward your goals.

If you don't have a financial advisor, we invite you to meet with an Edward Jones financial advisor to explore how to piece together your investments with purpose, resilience and a forward-looking, opportunistic mindset.

Strategic portfolio guidance

Defining your strategic investment allocations helps keep your portfolio aligned with your risk and return objectives, and we recommend taking a diversified approach. Our long-term strategic asset allocation guidance represents our view of balanced diversification for the fixed-income and equity portions of a well-diversified portfolio, based on our outlook for the economy and markets over the next 30 years. The exact weightings (neutral weights) to each asset class will depend on the broad allocation to equity and fixed-income investments that most closely aligns with your comfort with risk and financial goals.

Diversification does not ensure a profit or protect against loss in a declining market.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: U.S. large-cap stocks, international large-cap stocks, U.S. mid-cap stocks, U.S. small-cap stocks, international small- and mid-cap stocks, emerging-market equity.

Fixed-income diversification: U.S. investment-grade bonds, U.S. high-yield bonds, international bonds, emerging-market debt, cash.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: U.S. large-cap stocks, international large-cap stocks, U.S. mid-cap stocks, U.S. small-cap stocks, international small- and mid-cap stocks, emerging-market equity.

Fixed-income diversification: U.S. investment-grade bonds, U.S. high-yield bonds, international bonds, emerging-market debt, cash.

Opportunistic portfolio guidance

Our opportunistic portfolio guidance represents our timely investment advice based on current market conditions and a shorter-term outlook. We believe incorporating this guidance into a well-diversified portfolio may enhance your potential for greater returns without taking on unintentional risks, helping keep your portfolio aligned with your risk and return objectives. We recommend first considering our opportunistic asset allocation guidance to capture opportunities across asset classes. We then recommend considering opportunistic equity style, U.S. equity sector and U.S. investment-grade bond guidance for more supplemental portfolio positioning, if appropriate.

Our opportunistic asset allocation guidance follows:

Equity — overweight overall; overweight for U.S. large-cap stocks, U.S. mid-cap stocks, international small- and mid-cap stocks and emerging-market equity; neutral for U.S. small-cap stocks; underweight for international large-cap stocks.

Fixed income — underweight overall; neutral for emerging-market debt and cash; underweight for U.S. investment-grade bonds, U.S. high-yield bonds and international bonds.

Our opportunistic asset allocation guidance follows:

Equity — overweight overall; overweight for U.S. large-cap stocks, U.S. mid-cap stocks, international small- and mid-cap stocks and emerging-market equity; neutral for U.S. small-cap stocks; underweight for international large-cap stocks.

Fixed income — underweight overall; neutral for emerging-market debt and cash; underweight for U.S. investment-grade bonds, U.S. high-yield bonds and international bonds.

Our opportunistic equity style guidance is neutral for value-style equity and growth-style equity.

Our opportunistic equity style guidance is neutral for value-style equity and growth-style equity.

Our opportunistic equity sector guidance follows:

• Overweight for consumer discretionary and industrials

• Neutral for communication services, energy, financial services, health care, materials, real estate and technology

• Underweight for consumer staples and utilities

Our opportunistic equity sector guidance follows:

• Overweight for consumer discretionary and industrials

• Neutral for communication services, energy, financial services, health care, materials, real estate and technology

• Underweight for consumer staples and utilities

Our opportunistic U.S. investment-grade bond guidance is neutral in interest rate risk (duration) and credit risk.

Our opportunistic U.S. investment-grade bond guidance is neutral in interest rate risk (duration) and credit risk.

Brock Weimer

Brock Weimer is responsible for analyzing economic data, assessing market trends, and supporting the development of resources that help clients work toward their long-term financial goals.

Brock graduated from Southern Illinois University Edwardsville with a bachelor's degree in economics and finance. He is a CFA® charter holder and member of the CFA Institute and CFA Society of St. Louis.

Important information

Past performance of the markets is not a guarantee of future results.

Diversification does not ensure a profit or protect against loss in a declining market.

Investing in equities involves risk. The value of your shares will fluctuate, and you may lose principal. Mid- and small-cap stocks tend to be more volatile than large-company stocks. Special risks are involved in international and emerging-market investing, including those related to currency fluctuations and foreign political and economic events.

Rebalancing does not guarantee a profit or protect against loss and may result in a taxable event.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.

The opinions stated are as of the date of this report and for general information purposes only. This information is not directed to any specific investor or potential investor, and should not be interpreted as a specific recommendation or investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.