Tech Rotation, IPO Fever, and the Fed: 3 Drivers to Watch This Summer

Key takeaways

- Tech is cooling, not breaking: The recent pullback in semiconductors reflects profit-taking after a “too far, too fast” rally, with improving breadth signaling a healthier market backdrop. A potential U.S.–Iran deal could further support this broadening trend.

- IPO demand will test risk appetite: The SpaceX debut may act as a real-time gauge of investor sentiment and willingness to fund high-growth, capital-intensive businesses at elevated valuations. History suggests some caution after the initial excitement, as large IPOs have often underperformed the broader market over their first year.

- The Fed remains on hold: Elevated headline inflation is being driven largely by energy, while underlying pressures remain contained, giving policymakers room to stay patient.

- Expect volatility but stay invested: Markets appear to be transitioning toward broader leadership and more normal volatility, suggesting pullbacks are likely to be corrective rather than trend-ending.

Markets have entered the summer in a more volatile but we think still supportive phase, marked by shifting leadership, a highly anticipated IPO pipeline, and geopolitics coming back into focus, with a potential U.S. – Iran peace deal that could ease energy pressures.

After a historic rally in technology over the past two months, a wobble in semiconductor stocks disrupted the market’s recent calm, triggering a pullback in some of its biggest winners. Encouragingly, beneath the surface, dynamics have been improving, with early signs of rotation and broader participation. We think this shift could gain further traction if the Strait of Hormuz reopens, helping ease pressure on inflation and bond yields.

Here are three drivers to watch as we navigate the summer months:

1) Tech hits a speedbump: cooling after overheating

After a rapid two-month run in tech, particularly in AI-related stocks, investors have turned more cautious in early June. The semiconductor index, which had nearly doubled since the start of the year, pulled back about 12% before partially recovering later in the week. This move appears primarily driven by profit-taking following a parabolic rally, rather than any deterioration in fundamentals or a major setback in the AI narrative. Put simply, the group had moved too far, too fast.

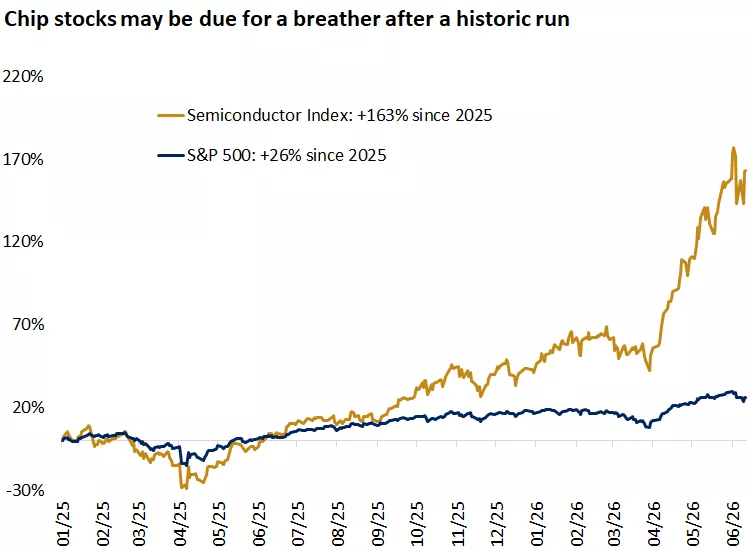

The graph shows the outperformance of semiconductors relative to the S&P 500 that reflect strong AI demand.

The graph shows the outperformance of semiconductors relative to the S&P 500 that reflect strong AI demand.

At the margin, reports pointing to a potential transition toward cheaper, more efficient AI models as business users become more cost-conscious, may lead to adjustments in AI workflows and a more measured pace of adoption. However, large cloud providers continue to ramp up infrastructure spending, reinforcing that the longer-term adoption trend remains intact.

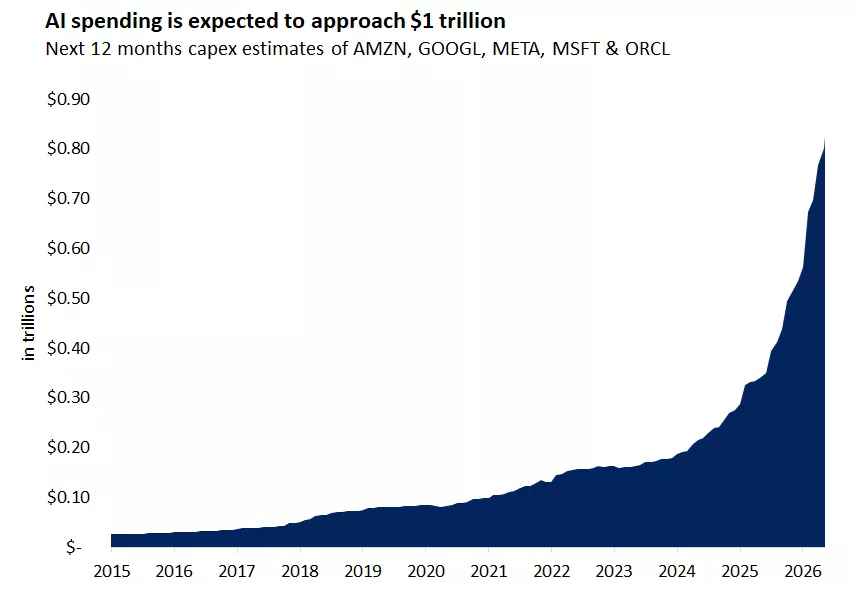

The graph shows that Amazon, Alphabet, Meta, Microsoft and Oracle are expected to spend almost one trillion dollars on AI infrastructure over the next 12 months.

The graph shows that Amazon, Alphabet, Meta, Microsoft and Oracle are expected to spend almost one trillion dollars on AI infrastructure over the next 12 months.

At the same time, as tech takes a breather, other sectors have begun to lead. The equal-weight S&P 500 is now outperforming its cap-weight counterpart year-to-date (11% vs. 9%), with financials, healthcare, defensives, and small-caps gaining traction. This points to broadening of leadership and participation, which we view as a healthy development for the durability of the bull market. We expect this trend to continue in the near term, particularly if progress toward reopening the Strait of Hormuz helps ease pressure on oil prices and bond yields.

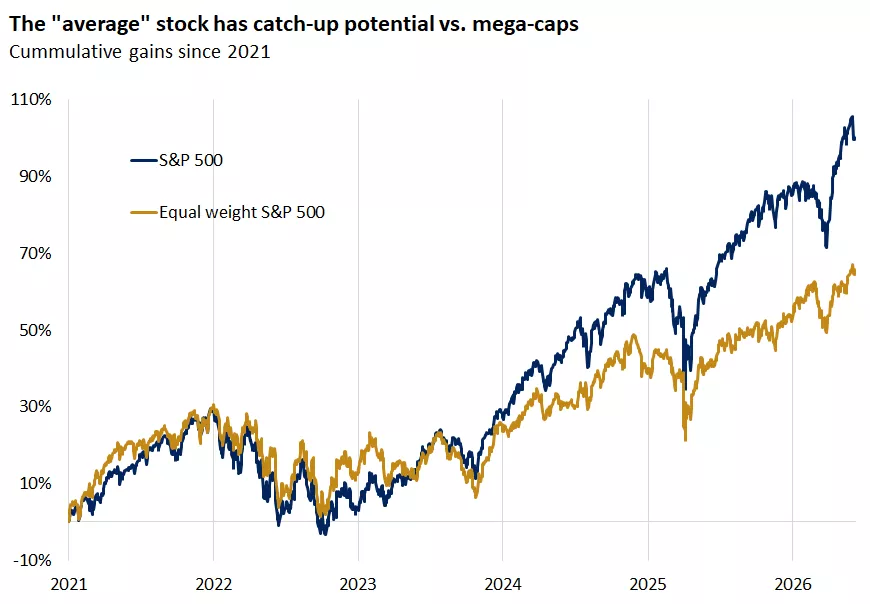

The graph shows the performance of the market-cap vs. equal weighted S&P 500. Despite excitement about AI, the equal weighted index is outperforming this year with perhaps more room for catch-up.

The graph shows the performance of the market-cap vs. equal weighted S&P 500. Despite excitement about AI, the equal weighted index is outperforming this year with perhaps more room for catch-up.

2) IPO activity: a real-time test of risk appetite

IPO activity is heating up, highlighted by the highly anticipated SpaceX debut, the largest public offering in history. The company raised approximately $75 billion, more than double the size of Saudi Aramco’s 2019 listing (the second largest), and at its $135 offer price was valued near $1.8 trillion, placing it among the largest companies globally.

Despite its size, only a small portion of shares is available for public trading. Founder holdings, insiders, and early investors retain the vast majority of ownership, leaving a free float of less than 5%. As a result, the company’s representation in major equity indices will be more limited than its headline valuation might suggest.

While some providers will fast-track inclusion, including indices such as the Russell 1000, MSCI U.S., and Nasdaq 100, creating early demand from passive investments, the S&P 500 has opted not to fast-track the stock, which will not be eligible to join the flagship index until a year after listing. This sets a precedent for how other large IPOs are treated going forward.

SpaceX is likely the first in a pipeline of mega-IPOs tied to AI and next-generation technologies, with companies such as Anthropic and OpenAI potentially following. This wave of supply raises a key question for markets: can demand keep pace? In that context, the SpaceX offering serves as a real-time test of risk appetite, in our view. We think strong demand would signal that investors remain willing to fund high-growth, capital-intensive businesses, with elevated valuations (SpaceX trades at more than 100 times its trailing revenue), while weaker demand could point to growing fatigue and tighter conditions for growth-oriented names.

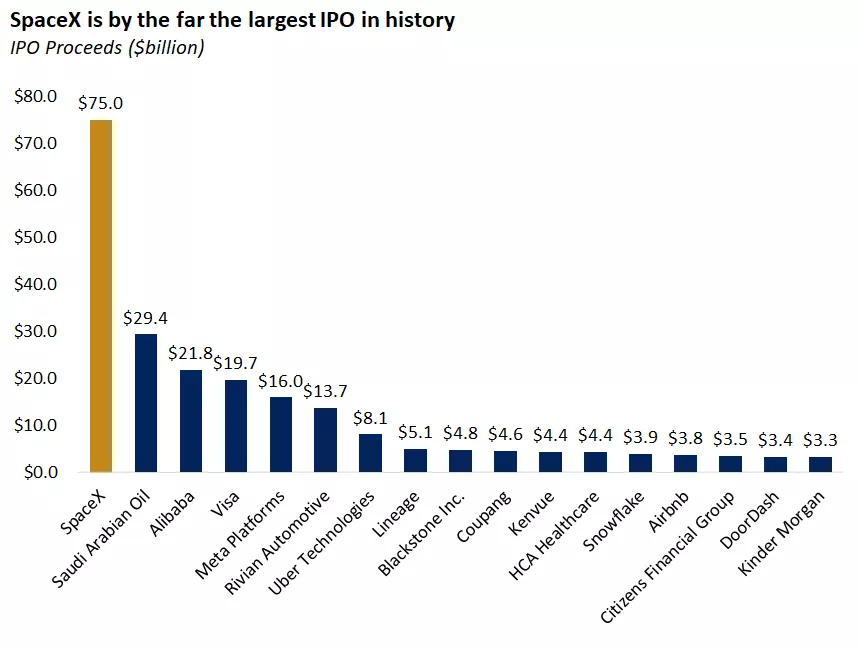

The graph shows that the SpaceX IPO is by far the largest in history in terms of money raised.

The graph shows that the SpaceX IPO is by far the largest in history in terms of money raised.

3) The Fed: balancing inflation signals with patience

The biggest shift in the macroeconomic outlook this year has been around the path of interest rates, driven by renewed inflation pressures. Following the jump in oil prices tied to Middle East tensions, bond markets have shifted from pricing in rate cuts to rate hikes.

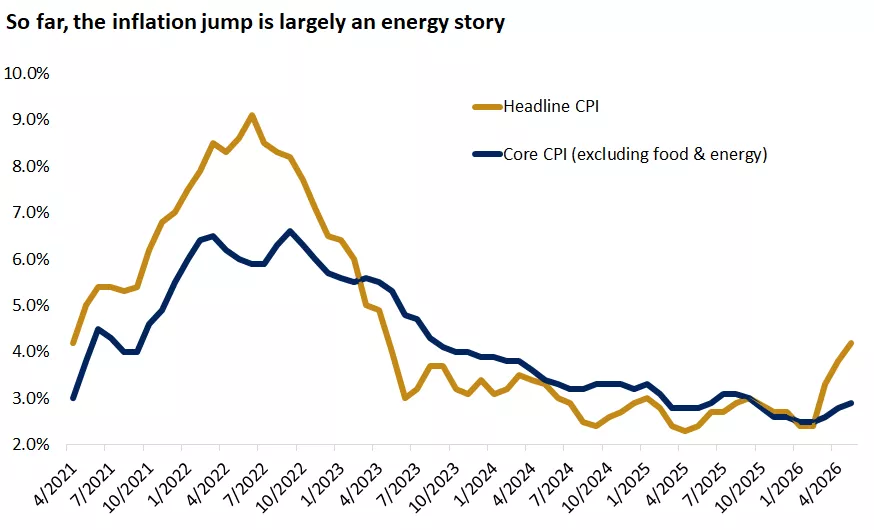

The May inflation data offered mixed signals for the Fed. Headline CPI rose 4.2% year-over-year, the highest since early 2023, largely reflecting higher energy prices. However, core CPI, which excludes food and energy, increased 2.9%, coming in slightly below expectations. Goods prices declined on a monthly basis for the first time in a year, suggesting that last year's tariff effects have faded, and services inflation showed no signs of a meaningful reacceleration.

Taken together, the data suggests that while headline inflation remains elevated, underlying pressures are more contained. We believe this gives the Fed some breathing room to remain patient as the energy shock works its way through the system. If oil prices stabilize or decline, as they have begun to do in June, we think inflation is likely to peak this quarter and ease into the back half of the year.

The near-term policy outlook remains murky, with the Fed expected to remove its easing bias at the upcoming meeting. Even so, we do not expect policymakers to respond aggressively to what appears to be largely energy-driven inflation. Instead, a prolonged pause remains the most likely outcome, in our view. For markets, a high-for-longer backdrop, rather than a shift back toward tightening, can still be supportive of valuations, in our view, particularly if it reflects stable economic growth and gradually easing inflation pressures.

The graph shows headline and core U.S. CPI, with the former jumping due to higher energy prices, while the latter has remained more tame.

The graph shows headline and core U.S. CPI, with the former jumping due to higher energy prices, while the latter has remained more tame.

Positioning for different scenarios including a potential summer "heat"

As markets often do, they tend to move in a “two steps forward, one step back” pattern. Following a strong two-month rally, it would not be surprising to us to see stocks pause over the summer to digest recent gains.

We do not view current conditions as signaling a breakdown. Rather, we see markets transitioning

- From narrow to broader leadership;

- From suppressed to more normal volatility; and

- From momentum-driven gains to a more mature phase of the cycle.

In the near term, this transition is likely to bring choppiness, particularly as leadership continues to evolve. However, with the economy resilient and earnings rising at a fast pace (second-quarter earnings are expected to grow 21%), we would expect any pullback to be corrective rather than indicative of a major peak or change in trend.

Against this backdrop, we recommend staying invested while being mindful of concentration in crowded segments. We would lean into broadening leadership, including cyclicals, U.S. mid-caps, and equal-weight exposure. While the U.S. economy continues to show the strongest momentum, a potential reopening of the Strait of Hormuz and the resulting decline in oil prices could provide relief for energy-sensitive regions, with international developed value stocks likely to benefit most, in our view.

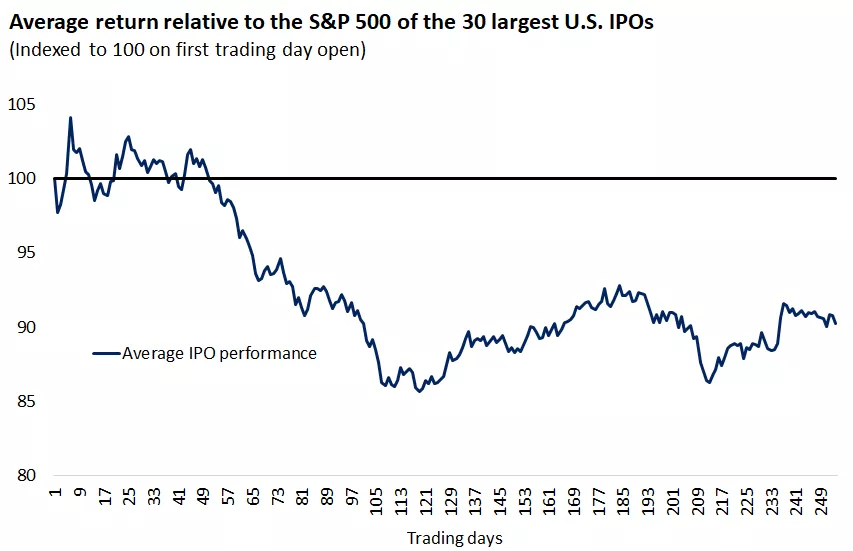

As it relates to IPOs, while each offering is unique, particularly at the scale of this year's listings, history suggests that early enthusiasm does not always translate into sustained outperformance. Among the 30 largest IPOs in the Russell 3000 over the past 20 years, companies have, on average, declined roughly 2.8% over the first three months following listing, while the S&P 500 gained about 3% over the same period. Over a longer horizon, these companies have underperformed the broader index by approximately 15% in their first year of trading. This reinforces the importance of selectivity and discipline. We recommend evaluating new opportunities based on fundamentals, valuation, and portfolio fit, rather than headlines and hype.

Overall, the summer “heat” may not come from a weakening market, but from shifting leadership and rising volatility. We remain constructive and would view pullbacks as opportunities to gradually add exposure and further diversify portfolios as the market evolves, based on your investment goals, risk tolerance and time horizon.

The graph shows the average first year relative to the S&P 500 performance of the largest 30 U.S. IPOs.

The graph shows the average first year relative to the S&P 500 performance of the largest 30 U.S. IPOs.

Angelo Kourkafas, CFA

Senior Global Investment Strategist

Sources for all data in commentary: Bloomberg, FactSet

Angelo Kourkafas

Angelo Kourkafas is responsible for analyzing market conditions, assessing economic trends and developing portfolio strategies and recommendations that help investors work toward their long-term financial goals.

He is a contributor to Edward Jones Market Insights and has been featured in The Wall Street Journal, CNBC, FORTUNE magazine, Marketwatch, U.S. News & World Report, The Observer and the Financial Post.

Angelo graduated magna cum laude with a bachelor’s degree in business administration from Athens University of Economics and Business in Greece and received an MBA with concentrations in finance and investments from Minnesota State University.

Previous weeks' weekly market wraps

Important Information:

The Weekly Market Update is published every Friday, after market close.

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Investors should understand the risks involved in owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss in declining markets.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent in international investing, including those related to currency fluctuations and foreign political and economic events.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.